You’ve found the perfect home. You’ve run the numbers. But then the question hits:

“Should I buy now with the minimum down payment… or keep saving until I’ve got the full 20%?”

On the other hand, waiting and saving more can result in lower payments and help avoid extra costs, such as mortgage insurance.

On one hand, jumping in sooner feels exciting — you get your home, start building equity, and stop paying rent.

If this sounds familiar, you’re not alone. It’s one of the most common dilemmas I hear from buyers across Canada. And here’s the thing — there’s no one-size-fits-all answer.

Both options come with their own set of advantages and trade-offs.

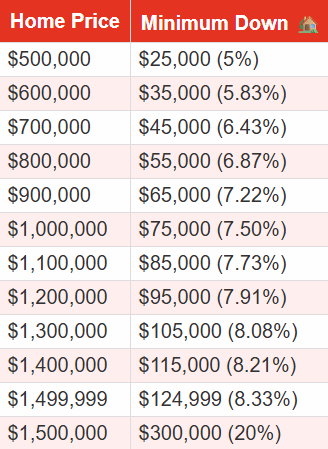

Minimum Down Payment Requirements in Canada:

Opting for the minimum down payment allows you to enter the market faster. You’re building equity right away and taking advantage of insured mortgage rates, which are typically 0.10–0.20% lower than conventional rates.

But the trade-off? You’ll carry a bigger mortgage, which means higher monthly payments, more interest costs over the life of the loan, and a higher income required to qualify. On top of that, you’ll need to pay CMHC insurance, which is added to your mortgage balance.

On the other hand, waiting until you have 20% means no CMHC premiums, lower overall interest costs, and stronger equity from day one.

The downside is it can take years to save that much, and during that time, home prices may climb faster than your savings — meaning you risk falling behind the market while you wait.

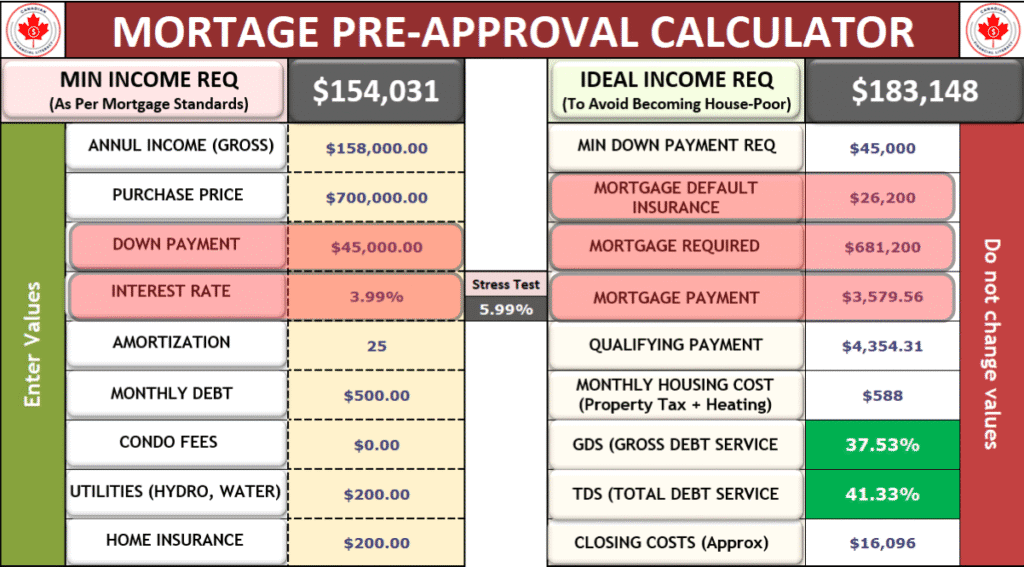

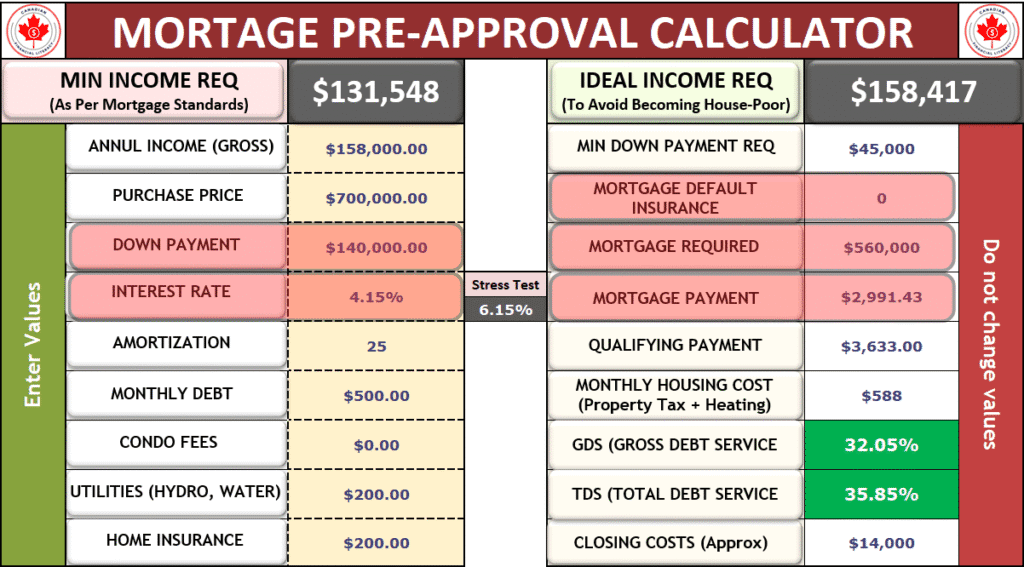

Real-Life Example: Buying a $700,000 Home

If you go with the minimum down payment, you’d put down $45,000. You’d also need to pay a CMHC insurance premium of $26,200, which is added to your mortgage.

With an insured mortgage rate of 3.99%, your monthly payment would be around $3,580. Because you’re borrowing more, the mortgage is bigger, which means higher interest costs over time and a higher income — roughly $154,000 gross — needed to qualify.

If you wait and save up 20%, your down payment would be $140,000, and you’d avoid CMHC insurance completely.

With a conventional mortgage rate of 4.15%, your monthly payment decreases to approximately $2,991, and the required income to qualify drops to around $131,500 gross. You also pay less interest over the life of the mortgage and start with more equity in your home.

So, Which Option Should You Choose?

If your goal is to enter the market sooner and you’re willing to pay CMHC premiums, the minimum down payment may be the right choice.

If you want to avoid extra costs and can save more, waiting until you have 20% down could be smarter.

At the end of the day, the best choice depends on your timeline, income, savings strategy, and comfort with risk.

Want help running your own numbers? Download my Home Buying Planner.

Ready To Buy A Home In Canada?

You are just one step away from confidently making a well-informed home-buying decision.